Page 218 - Accountancy_F5

P. 218

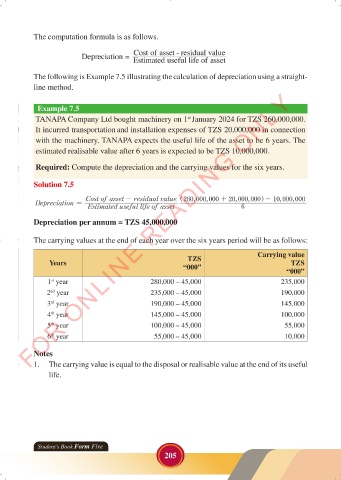

The computation formula is as follows.

Cost of asset residual value-

Depreciation =

Estimated useful life of asset

The following is Example 7.5 illustrating the calculation of depreciation using a straight-

line method.

FOR ONLINE READING ONLY

Example 7.5

TANAPA Company Ltd bought machinery on 1 January 2024 for TZS 260,000,000.

st

LANGUAGE EDITING

It incurred transportation and installation expenses of TZS 20,000,000 in connection

LANGUAGE EDITING

with the machinery. TANAPA expects the useful life of the asset to be 6 years. The

estimated realisable value after 6 years is expected to be TZS 10,000,000.

Required: Compute the depreciation and the carrying values for the six years.

Solution 7.5

Cost of asset - residual value ^ 260 ,000 000 + 20 ,000 000 - 10 ,000 000

,

,

,

h

Depreciation =

Estimated useful life of asset 6

Depreciation per annum = TZS 45,000,000

The carrying values at the end of each year over the six years period will be as follows:

Carrying value

Years TZS TZS

“000”

“000”

1 year 280,000 – 45,000 235,000

st

2 year 235,000 – 45,000 190,000

nd

3 year 190,000 – 45,000 145,000

rd

4 year 145,000 – 45,000 100,000

th

5 year 100,000 – 45,000 55,000

th

6 year 55,000 – 45,000 10,000

th

Notes

1. The carrying value is equal to the disposal or realisable value at the end of its useful

life.

Student’s Book Form Five

205

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 205 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 205