Page 221 - Accountancy_F5

P. 221

It is suitable for assets which give the It is suitable for assets which give a higher

same efficiency year after year example efficiency in earlier years and a lower

a building is used equally over the years. efficiency in later years, example machinery

used in various manufacturing processes and

motor vehicles

FOR ONLINE READING ONLY

If repairs increase in later years, the charge The charge of depreciation plus repairs is

of depreciation plus repairs increase each expected to be the same over the years.

year (since the depreciation is constant). In the initial years when repairs are low,

depreciation is high, and in later years when

LANGUAGE EDITING

repairs are high, depreciation is low.

It is simple to understand and apply. It is relatively difficult to understand and

apply.

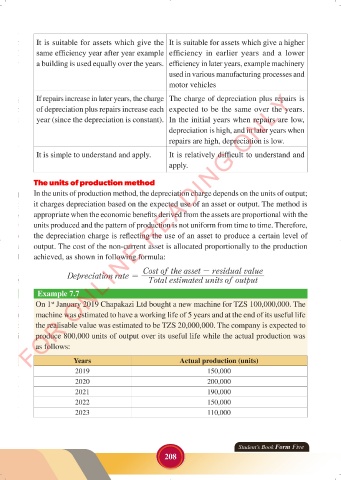

The units of production method

In the units of production method, the depreciation charge depends on the units of output;

it charges depreciation based on the expected use of an asset or output. The method is

appropriate when the economic benefits derived from the assets are proportional with the

units produced and the pattern of production is not uniform from time to time. Therefore,

the depreciation charge is reflecting the use of an asset to produce a certain level of

output. The cost of the non-current asset is allocated proportionally to the production

achieved, as shown in following formula:

Cost of the asset - residual value

Depreciation rate =

Total estimated units of output

Example 7.7

On 1 January 2019 Chapakazi Ltd bought a new machine for TZS 100,000,000. The

st

machine was estimated to have a working life of 5 years and at the end of its useful life

the realisable value was estimated to be TZS 20,000,000. The company is expected to

produce 800,000 units of output over its useful life while the actual production was

as follows:

Years Actual production (units)

2019 150,000

2020 200,000

2021 190,000

2022 150,000

2023 110,000

Student’s Book Form Five

208

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 208

ACCOUNTANCY_DUMMY_23 JUNE.indd 208 23/06/2024 17:35