Page 219 - Accountancy_F5

P. 219

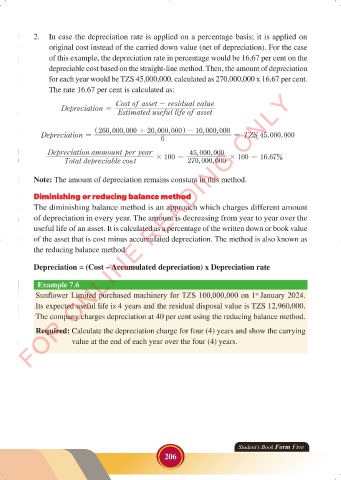

2. In case the depreciation rate is applied on a percentage basis; it is applied on

original cost instead of the carried down value (net of depreciation). For the case

of this example, the depreciation rate in percentage would be 16.67 per cent on the

depreciable cost based on the straight-line method. Then, the amount of depreciation

for each year would be TZS 45,000,000, calculated as 270,000,000 x 16.67 per cent.

The rate 16.67 per cent is calculated as:

FOR ONLINE READING ONLY

Cost of asset - residual value

Depreciation =

Estimated useful life of asset

,

,

,

^ 260 ,000 000 + 20 ,000 000 - 10 ,000 000

h

Depreciation = = TZS 45 ,000 000

,

LANGUAGE EDITING

6

,

Depreciation ammount per year 45 ,000 000

.%

,

Total depreciable cost # 100 = 270 ,000 000 # 100 = 16 67

Note: The amount of depreciation remains constant in this method.

Diminishing or reducing balance method

The diminishing balance method is an approach which charges different amount

of depreciation in every year. The amount is decreasing from year to year over the

useful life of an asset. It is calculated as a percentage of the written down or book value

of the asset that is cost minus accumulated depreciation. The method is also known as

the reducing balance method.

Depreciation = (Cost – Accumulated depreciation) x Depreciation rate

Example 7.6

Sunflower Limited purchased machinery for TZS 100,000,000 on 1 January 2024.

st

Its expected useful life is 4 years and the residual disposal value is TZS 12,960,000.

The company charges depreciation at 40 per cent using the reducing balance method.

Required: Calculate the depreciation charge for four (4) years and show the carrying

value at the end of each year over the four (4) years.

Student’s Book Form Five

206

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 206 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 206