Page 256 - Accountancy_F5

P. 256

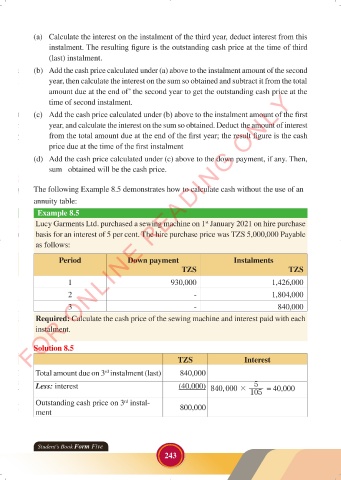

(a) Calculate the interest on the instalment of the third year, deduct interest from this

instalment. The resulting figure is the outstanding cash price at the time of third

(last) instalment.

(b) Add the cash price calculated under (a) above to the instalment amount of the second

year, then calculate the interest on the sum so obtained and subtract it from the total

FOR ONLINE READING ONLY

amount due at the end of’ the second year to get the outstanding cash price at the

time of second instalment.

(c) Add the cash price calculated under (b) above to the instalment amount of the first

LANGUAGE EDITING

year, and calculate the interest on the sum so obtained. Deduct the amount of interest

from the total amount due at the end of the first year; the result figure is the cash

LANGUAGE EDITING

price due at the time of the first instalment

(d) Add the cash price calculated under (c) above to the down payment, if any. Then,

sum obtained will be the cash price.

The following Example 8.5 demonstrates how to calculate cash without the use of an

annuity table:

Example 8.5

Lucy Garments Ltd. purchased a sewing machine on 1 January 2021 on hire purchase

st

basis for an interest of 5 per cent. The hire purchase price was TZS 5,000,000 Payable

as follows:

Period Down payment Instalments

TZS TZS

1 930,000 1,426,000

2 - 1,804,000

3 - 840,000

Required: Calculate the cash price of the sewing machine and interest paid with each

instalment.

Solution 8.5

TZS Interest

Total amount due on 3 instalment (last) 840,000

rd

Less: interest (40,000) 840 ,000 # 5 = 40,000

105

Outstanding cash price on 3 instal- 800,000

rd

ment

Student’s Book Form Five

243

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 243 23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 243