Page 257 - Accountancy_F5

P. 257

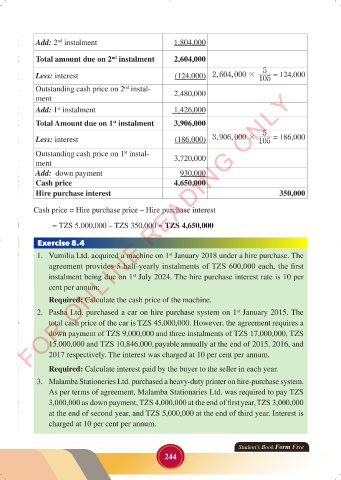

Add: 2 instalment 1,804,000

nd

Total amount due on 2 instalment 2,604,000

nd

5

,

Less: interest (124,000) ,2 604 000 # 105 = 124,000

Outstanding cash price on 2 instal- 2,480,000

nd

FOR ONLINE READING ONLY

ment

Add: 1 instalment 1,426,000

st

Total Amount due on 1 instalment 3,906,000

st

5

,

Less: interest (186,000) ,3 906 000 # 105 = 186,000

LANGUAGE EDITING

Outstanding cash price on 1 instal- 3,720,000

st

ment

Add: down payment 930,000

Cash price 4,650,000

Hire purchase interest 350,000

Cash price = Hire purchase price – Hire purchase interest

= TZS 5,000,000 – TZS 350,000 = TZS 4,650,000

Exercise 8.4

1. Vumilia Ltd. acquired a machine on 1 January 2018 under a hire purchase. The

st

agreement provides 5 half-yearly instalments of TZS 600,000 each, the first

instalment being due on 1 July 2024. The hire purchase interest rate is 10 per

st

cent per annum:

Required: Calculate the cash price of the machine.

2. Pasha Ltd. purchased a car on hire purchase system on 1 January 2015. The

st

total cash price of the car is TZS 45,000,000. However, the agreement requires a

down payment of TZS 9,000,000 and three instalments of TZS 17,000,000, TZS

15,000,000 and TZS 10,846,000, payable annually at the end of 2015, 2016, and

2017 respectively. The interest was charged at 10 per cent per annum.

Required: Calculate interest paid by the buyer to the seller in each year.

3. Malamba Stationeries Ltd. purchased a heavy-duty printer on hire-purchase system.

As per terms of agreement, Malamba Stationaries Ltd. was required to pay TZS

3,000,000 as down payment, TZS 4,000,000 at the end of first year, TZS 3,000,000

at the end of second year, and TZS 5,000,000 at the end of third year. Interest is

charged at 10 per cent per annum.

Student’s Book Form Five

244

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 244 23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 244