Page 258 - Accountancy_F5

P. 258

Required: Calculate the total cash price of the printer and interest paid with each

instalment.

Accounting entries for recording hire purchase transactions

Accounting for hire purchase transactions involves recording the acquisition of an asset,

FOR ONLINE READING ONLY

recognizing the corresponding liability, and subsequently accounting for interest and

periodic payments. The following is step-by-step guide on the accounting entries for

recording hire purchase transactions between parties:

LANGUAGE EDITING

Accounting entries in the books of hire purchaser

LANGUAGE EDITING

When the asset is purchased on hire purchase, it is assumed that the purchaser has full

intention of paying all the instalments. It is believed that hire purchase is just a method

of financing non-current assets. In this situation, on purchase of non-current assets, the

respective non-current asset account is debited with the total amount of cash price, and

the corresponding credit is given to hire vendor’s account. On the contrary, interest is

recognised and accounted for at the time when instalments become due by debiting the

interest account and crediting the hire vendor’s account.

For the purpose of accounting for initial cash down payment and annual instalments,

the hire vendor’s account is debited on the relevant date and crediting the bank/cash

account. The following are accounting entries in the books of hire purchaser.

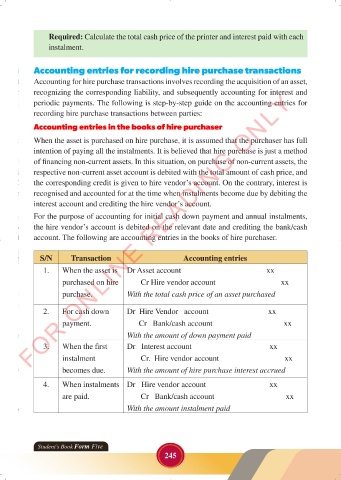

S/N Transaction Accounting entries

1. When the asset is Dr Asset account xx

purchased on hire Cr Hire vendor account xx

purchase. With the total cash price of an asset purchased

2. For cash down Dr Hire Vendor account xx

payment. Cr Bank/cash account xx

With the amount of down payment paid

3. When the first Dr Interest account xx

instalment Cr. Hire vendor account xx

becomes due. With the amount of hire purchase interest accrued

4. When instalments Dr Hire vendor account xx

are paid. Cr Bank/cash account xx

With the amount instalment paid

Student’s Book Form Five

245

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 245

ACCOUNTANCY_DUMMY_23 JUNE.indd 245 23/06/2024 17:36