Page 261 - Accountancy_F5

P. 261

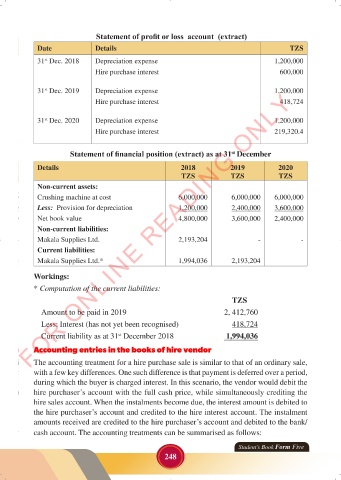

Statement of profit or loss account (extract)

Date Details TZS

31 Dec. 2018 Depreciation expense 1,200,000

st

Hire purchase interest 600,000

FOR ONLINE READING ONLY

31 Dec. 2019 Depreciation expense 1,200,000

st

Hire purchase interest 418,724

31 Dec. 2020 Depreciation expense 1,200,000

st

Hire purchase interest 219,320.4

LANGUAGE EDITING

Statement of financial position (extract) as at 31 December

st

Details 2018 2019 2020

TZS TZS TZS

Non-current assets:

Crushing machine at cost 6,000,000 6,000,000 6,000,000

Less: Provision for depreciation 1,200,000 2,400,000 3,600,000

Net book value 4,800,000 3,600,000 2,400,000

Non-current liabilities:

Makala Supplies Ltd. 2,193,204 - -

Current liabilities:

Makala Supplies Ltd.* 1,994,036 2,193,204

Workings:

* Computation of the current liabilities:

TZS

Amount to be paid in 2019 2, 412,760

Less: Interest (has not yet been recognised) 418,724

Current liability as at 31 December 2018 1,994,036

st

Accounting entries in the books of hire vendor

The accounting treatment for a hire purchase sale is similar to that of an ordinary sale,

with a few key differences. One such difference is that payment is deferred over a period,

during which the buyer is charged interest. In this scenario, the vendor would debit the

hire purchaser’s account with the full cash price, while simultaneously crediting the

hire sales account. When the instalments become due, the interest amount is debited to

the hire purchaser’s account and credited to the hire interest account. The instalment

amounts received are credited to the hire purchaser’s account and debited to the bank/

cash account. The accounting treatments can be summarised as follows:

Student’s Book Form Five

248

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 248 23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 248