Page 264 - Accountancy_F5

P. 264

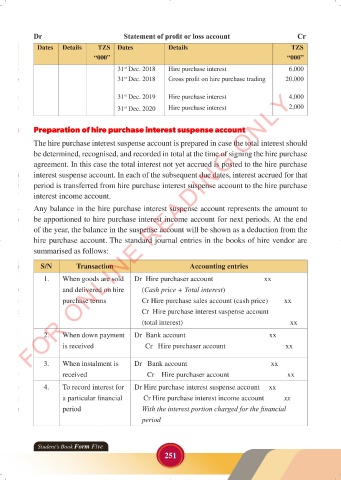

Dr Statement of profit or loss account Cr

Dates Details TZS Dates Details TZS

“000” “000”

31 Dec. 2018 Hire purchase interest 6,000

st

31 Dec. 2018 Gross profit on hire purchase trading 20,000

st

FOR ONLINE READING ONLY

31 Dec. 2019 Hire purchase interest 4,000

st

31 Dec. 2020 Hire purchase interest 2,000

st

LANGUAGE EDITING

Preparation of hire purchase interest suspense account

LANGUAGE EDITING

The hire purchase interest suspense account is prepared in case the total interest should

be determined, recognised, and recorded in total at the time of signing the hire purchase

agreement. In this case the total interest not yet accrued is posted to the hire purchase

interest suspense account. In each of the subsequent due dates, interest accrued for that

period is transferred from hire purchase interest suspense account to the hire purchase

interest income account.

Any balance in the hire purchase interest suspense account represents the amount to

be apportioned to hire purchase interest income account for next periods. At the end

of the year, the balance in the suspense account will be shown as a deduction from the

hire purchase account. The standard journal entries in the books of hire vendor are

summarised as follows:

S/N Transaction Accounting entries

1. When goods are sold Dr Hire purchaser account xx

and delivered on hire (Cash price + Total interest)

purchase terms Cr Hire purchase sales account (cash price) xx

Cr Hire purchase interest suspense account

(total interest) xx

2. When down payment Dr Bank account xx

is received Cr Hire purchaser account xx

3. When instalment is Dr Bank account xx

received Cr Hire purchaser account xx

4. To record interest for Dr Hire purchase interest suspense account xx

a particular financial Cr Hire purchase interest income account xx

period With the interest portion charged for the financial

period

Student’s Book Form Five

251

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 251 23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 251