Page 55 - Accountancy_F5

P. 55

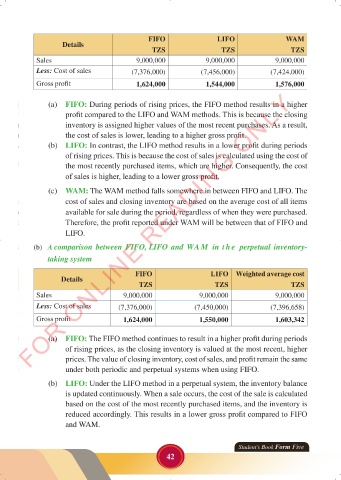

FIFO LIFO WAM

Details

TZS TZS TZS

Sales 9,000,000 9,000,000 9,000,000

Less: Cost of sales (7,376,000) (7,456,000) (7,424,000)

Gross profit 1,624,000 1,544,000 1,576,000

FOR ONLINE READING ONLY

(a) FIFO: During periods of rising prices, the FIFO method results in a higher

profit compared to the LIFO and WAM methods. This is because the closing

inventory is assigned higher values of the most recent purchases. As a result,

the cost of sales is lower, leading to a higher gross profit.

LANGUAGE EDITING

(b) LIFO: In contrast, the LIFO method results in a lower profit during periods

of rising prices. This is because the cost of sales is calculated using the cost of

the most recently purchased items, which are higher. Consequently, the cost

of sales is higher, leading to a lower gross profit.

(c) WAM: The WAM method falls somewhere in between FIFO and LIFO. The

cost of sales and closing inventory are based on the average cost of all items

available for sale during the period, regardless of when they were purchased.

Therefore, the profit reported under WAM will be between that of FIFO and

LIFO.

(b) A comparison between FIFO, LIFO and WA M in t h e perpetual inventory-

taking system

FIFO LIFO Weighted average cost

Details

TZS TZS TZS

Sales 9,000,000 9,000,000 9,000,000

Less: Cost of sales (7,376,000) (7,450,000) (7,396,658)

Gross profit 1,624,000 1,550,000 1,603,342

(a) FIFO: The FIFO method continues to result in a higher profit during periods

of rising prices, as the closing inventory is valued at the most recent, higher

prices. The value of closing inventory, cost of sales, and profit remain the same

under both periodic and perpetual systems when using FIFO.

(b) LIFO: Under the LIFO method in a perpetual system, the inventory balance

is updated continuously. When a sale occurs, the cost of the sale is calculated

based on the cost of the most recently purchased items, and the inventory is

reduced accordingly. This results in a lower gross profit compared to FIFO

and WAM.

Student’s Book Form Five

42

23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 42

ACCOUNTANCY_DUMMY_23 JUNE.indd 42 23/06/2024 17:34