Page 53 - Accountancy_F5

P. 53

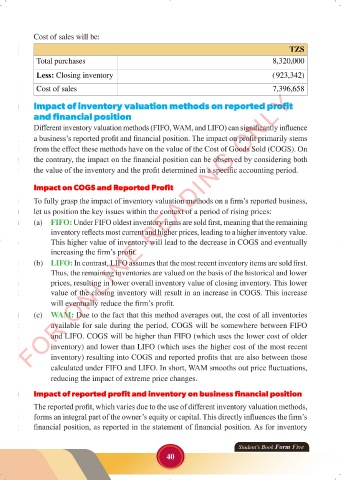

Cost of sales will be:

TZS

Total purchases 8,320,000

Less: Closing inventory (923,342)

Cost of sales 7,396,658

FOR ONLINE READING ONLY

Impact of inventory valuation methods on reported profit

and financial position

Different inventory valuation methods (FIFO, WAM, and LIFO) can significantly influence

a business’s reported profit and financial position. The impact on profit primarily stems

LANGUAGE EDITING

from the effect these methods have on the value of the Cost of Goods Sold (COGS). On

the contrary, the impact on the financial position can be observed by considering both

the value of the inventory and the profit determined in a specific accounting period.

Impact on COGS and Reported Profit

To fully grasp the impact of inventory valuation methods on a firm’s reported business,

let us position the key issues within the context of a period of rising prices:

(a) FIFO: Under FIFO oldest inventory items are sold first, meaning that the remaining

inventory reflects most current and higher prices, leading to a higher inventory value.

This higher value of inventory will lead to the decrease in COGS and eventually

increasing the firm’s profit.

(b) LIFO: In contrast, LIFO assumes that the most recent inventory items are sold first.

Thus, the remaining inventories are valued on the basis of the historical and lower

prices, resulting in lower overall inventory value of closing inventory. This lower

value of the closing inventory will result in an increase in COGS. This increase

will eventually reduce the firm’s profit.

(c) WAM: Due to the fact that this method averages out, the cost of all inventories

available for sale during the period, COGS will be somewhere between FIFO

and LIFO. COGS will be higher than FIFO (which uses the lower cost of older

inventory) and lower than LIFO (which uses the higher cost of the most recent

inventory) resulting into COGS and reported profits that are also between those

calculated under FIFO and LIFO. In short, WAM smooths out price fluctuations,

reducing the impact of extreme price changes.

Impact of reported profit and inventory on business financial position

The reported profit, which varies due to the use of different inventory valuation methods,

forms an integral part of the owner’s equity or capital. This directly influences the firm’s

financial position, as reported in the statement of financial position. As for inventory

Student’s Book Form Five

40

23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 40 23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 40