Page 49 - Accountancy_F5

P. 49

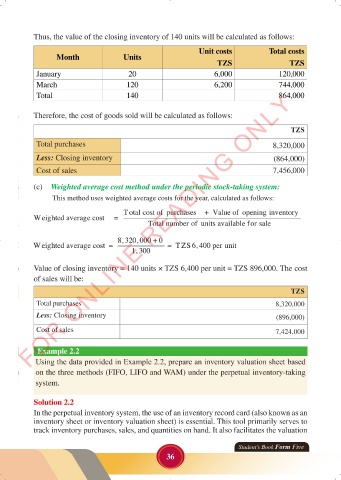

Thus, the value of the closing inventory of 140 units will be calculated as follows:

Unit costs Total costs

Month Units

TZS TZS

January 20 6,000 120,000

March 120 6,200 744,000

FOR ONLINE READING ONLY

Total 140 864,000

Therefore, the cost of goods sold will be calculated as follows:

TZS

LANGUAGE EDITING

Total purchases 8,320,000

Less: Closing inventory (864,000)

Cost of sales 7,456,000

(c) Weighted average cost method under the periodic stock-taking system:

This method uses weighted average costs for the year, calculated as follows:

Value of closing inventory = 140 units × TZS 6,400 per unit = TZS 896,000. The cost

of sales will be:

TZS

Total purchases 8,320,000

Less: Closing inventory (896,000)

Cost of sales 7,424,000

Example 2.2

Using the data provided in Example 2.2, prepare an inventory valuation sheet based

on the three methods (FIFO, LIFO and WAM) under the perpetual inventory-taking

system.

Solution 2.2

In the perpetual inventory system, the use of an inventory record card (also known as an

inventory sheet or inventory valuation sheet) is essential. This tool primarily serves to

track inventory purchases, sales, and quantities on hand. It also facilitates the valuation

Student’s Book Form Five

36

23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 36 23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 36