Page 47 - Accountancy_F5

P. 47

Which inventory valuation regardless of the particular approach used in

method to choose? practice, knowing how each of them reports

will offer a thorough understanding of the

The selection of an inventory valuation reasoning behind inventory management

method is influenced by several factors, approaches. To fully comprehend inventory

including the nature of the business, price value and how it affects financial reporting,

FOR ONLINE READING ONLY

volatility, and the entity’s financial reporting you must have a wide understanding of the

obligations. Among these, the financial subject.

reporting requirements are particularly

important. For instance, IAS 2 does not Applying the three methods

permit the use of LIFO method. In Tanzania, of inventory valuation

LANGUAGE EDITING

where accounting practices generally After understanding the theories and

adhere to IFRS and IAS, businesses are principles behind the three inventory

not expected to use LIFO in their financial valuation methods, it is equally important

reporting. to comprehend their practical application.

Thus, all of the inventory valuation Let us proceed with Example 2.1, which

techniques: FIFO, LIFO, and WAM, should demonstrates their use in a scenario that

be understood, though. That being said, mirrors real-world business operations.

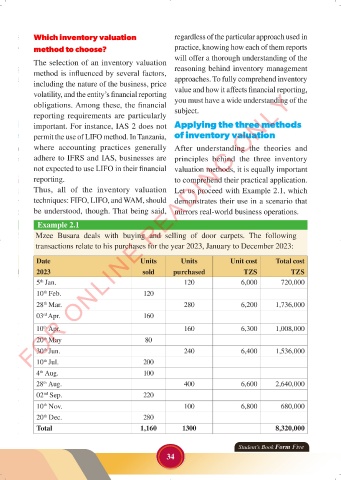

Example 2.1

Mzee Busara deals with buying and selling of door carpets. The following

transactions relate to his purchases for the year 2023, January to December 2023:

Date Units Units Unit cost Total cost

2023 sold purchased TZS TZS

5 Jan. 120 6,000 720,000

th

10 Feb. 120

th

28 Mar. 280 6,200 1,736,000

th

03 Apr. 160

rd

10 Apr. 160 6,300 1,008,000

th

20 May 80

th

30 Jun. 240 6,400 1,536,000

th

10 Jul. 200

th

4 Aug. 100

th

28 Aug. 400 6,600 2,640,000

th

02 Sep. 220

nd

10 Nov. 100 6,800 680,000

th

20 Dec. 280

th

Total 1,160 1300 8,320,000

Student’s Book Form Five

34

23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 34

ACCOUNTANCY_DUMMY_23 JUNE.indd 34 23/06/2024 17:34