Page 50 - Accountancy_F5

P. 50

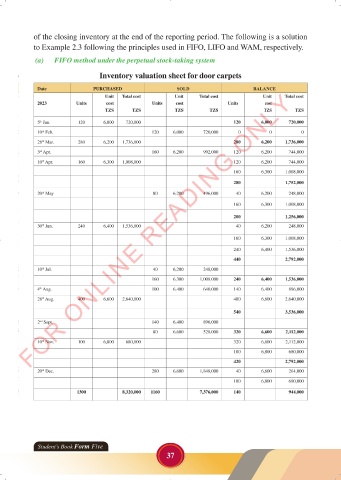

of the closing inventory at the end of the reporting period. The following is a solution

to Example 2.3 following the principles used in FIFO, LIFO and WAM, respectively.

(a) FIFO method under the perpetual stock-taking system

Inventory valuation sheet for door carpets

Date PURCHASED SOLD BALANCE

FOR ONLINE READING ONLY

Unit Total cost Unit Total cost Unit Total cost

2023 Units cost Units cost Units cost

TZS TZS TZS TZS TZS TZS

5 Jan. 120 6,000 720,000 120 6,000 720,000

th

10 Feb. 120 6,000 720,000 0 0 0

th

LANGUAGE EDITING

28 Mar. 280 6,200 1,736,000 280 6,200 1,736,000

th

3 Apr. 160 6,200 992,000 120 6,200 744,000

rd

10 Apr. 160 6,300 1,008,000 120 6,200 744,000

th

160 6,300 1,008,000

280 1,752,000

20 May 80 6,200 496,000 40 6,200 248,000

th

160 6,300 1,008,000

200 1,256,000

240

6,400

40

6,200

1,536,000

th

30 Jun. LANGUAGE EDITING 248,000

160 6,300 1,008,000

240 6,400 1,536,000

440 2,792,000

10 Jul. 40 6,200 248,000

th

160 6,300 1,008,000 240 6,400 1,536,000

4 Aug. 100 6,400 640,000 140 6,400 896,000

th

28 Aug. 400 6,600 2,640,000 400 6,600 2,640,000

th

540 3,536,000

2 Sept. 140 6,400 896,000

nd

80 6,600 528,000 320 6,600 2,112,000

th

10 Nov. 100 6,800 680,000 320 6,600 2,112,000

100 6,800 680,000

420 2,792,000

20 Dec. 280 6,600 1,848,000 40 6,600 264,000

th

100 6,800 680,000

1300 8,320,000 1160 7,376,000 140 944,000

Student’s Book Form Five

37

23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 37

ACCOUNTANCY_DUMMY_23 JUNE.indd 37 23/06/2024 17:34