Page 52 - Accountancy_F5

P. 52

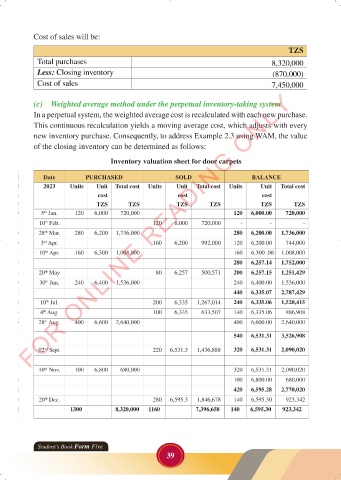

Cost of sales will be:

TZS

Total purchases 8,320,000

Less: Closing inventory (870,000)

Cost of sales 7,450,000

th FOR ONLINE READING ONLY

(c) Weighted average method under the perpetual inventory-taking system

In a perpetual system, the weighted average cost is recalculated with each new purchase.

This continuous recalculation yields a moving average cost, which adjusts with every

new inventory purchase. Consequently, to address Example 2.3 using WAM, the value

LANGUAGE EDITING

of the closing inventory can be determined as follows:

Inventory valuation sheet for door carpets

Date PURCHASED SOLD BALANCE

2023 Units Unit Total cost Units Unit Total cost Units Unit Total cost

cost cost cost

TZS TZS TZS TZS TZS TZS

5 Jan. 120 6,000 720,000 120 6,000.00 720,000

th

120

-

6,000

10 Feb. LANGUAGE EDITING -

-

720,000

th

28 Mar. 280 6,200 1,736,000 280 6,200.00 1,736,000

th

3 Apr. 160 6,200 992,000 120 6,200.00 744,000

rd

10 Apr. 160 6,300 1,008,000 160 6,300 .00 1,008,000

th

280 6,257.14 1,752,000

20 May 80 6,257 500,571 200 6,257.15 1,251,429

th

30 Jun. 240 6,400 1,536,000 240 6,400.00 1,536,000

th

440 6,335.07 2,787,429

10 Jul. 200 6,335 1,267,014 240 6,335.06 1,520,415

th

4 Aug. 100 6,335 633,507 140 6,335.06 886,908

th

28 Aug. 400 6,600 2,640,000 400 6,600.00 2,640,000

th

540 6,531.31 3,526,908

nd

02 Sept. 220 6,531.3 1,436,888 320 6,531.31 2,090,020

10 Nov. 100 6,800 680,000 320 6,531.31 2,090,020

100 6,800.00 680,000

420 6,595.28 2,770,020

th

20 Dec. 280 6,595.3 1,846,678 140 6,595.30 923,342

1300 8,320,000 1160 7,396,658 140 6,595.30 923,342

Student’s Book Form Five

39

23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 39 23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 39