Page 83 - Accountancy_F5

P. 83

The entire project was financed by a bank loan. Interest, advertising and other expenses

totalled TZS 1,000,000. Loss of TZS 70,000 was discovered. It was also discovered

by a consultant that Edward used FIFO method for valuing unsold inventory whereas

Hamdani used weighted average cost method for the same purpose.

Required: Prepare separate statements of profit or loss for the two brothers clearly

FOR ONLINE READING ONLY

showing your computations of closing inventory in each case.

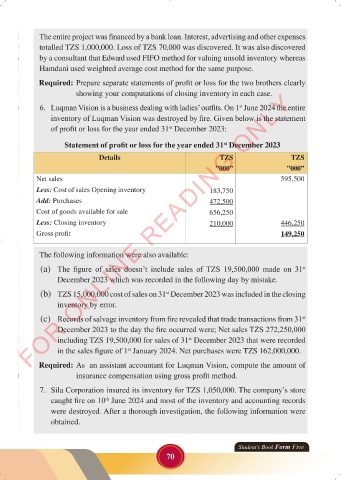

6. Luqman Vision is a business dealing with ladies’ outfits. On 1 June 2024 the entire

st

inventory of Luqman Vision was destroyed by fire. Given below is the statement

of profit or loss for the year ended 31 December 2023:

st

LANGUAGE EDITING

Statement of profit or loss for the year ended 31 December 2023

st

Details TZS TZS

”000” ”000”

Net sales 595,500

Less: Cost of sales Opening inventory 183,750

Add: Purchases 472,500

Cost of goods available for sale 656,250

Less: Closing inventory 210,000 446,250

Gross profit 149,250

The following information were also available:

(a) The figure of sales doesn’t include sales of TZS 19,500,000 made on 31 st

December 2023 which was recorded in the following day by mistake.

(b) TZS 15,000,000 cost of sales on 31 December 2023 was included in the closing

st

inventory by error.

(c) Records of salvage inventory from fire revealed that trade transactions from 31

st

December 2023 to the day the fire occurred were; Net sales TZS 272,250,000

including TZS 19,500,000 for sales of 31 December 2023 that were recorded

st

in the sales figure of 1 January 2024. Net purchases were TZS 162,000,000.

st

Required: As an assistant accountant for Luqman Vision, compute the amount of

insurance compensation using gross profit method.

7. Sila Corporation insured its inventory for TZS 1,050,000. The company’s store

caught fire on 10 June 2024 and most of the inventory and accounting records

th

were destroyed. After a thorough investigation, the following information were

obtained.

Student’s Book Form Five

70

ACCOUNTANCY_DUMMY_23 JUNE.indd 70 23/06/2024 17:35

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 70