Page 85 - Accountancy_F5

P. 85

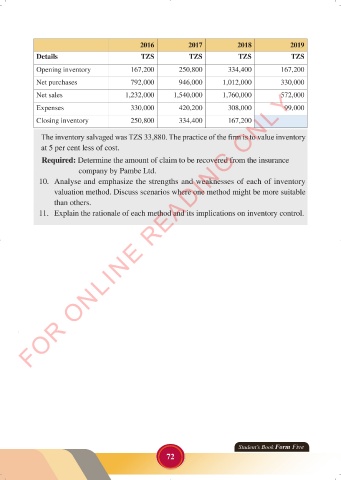

2016 2017 2018 2019

Details TZS TZS TZS TZS

Opening inventory 167,200 250,800 334,400 167,200

Net purchases 792,000 946,000 1,012,000 330,000

FOR ONLINE READING ONLY

Net sales 1,232,000 1,540,000 1,760,000 572,000

Expenses 330,000 420,200 308,000 99,000

Closing inventory 250,800 334,400 167,200

The inventory salvaged was TZS 33,880. The practice of the firm is to value inventory

LANGUAGE EDITING

at 5 per cent less of cost.

Required: Determine the amount of claim to be recovered from the insurance

company by Pambe Ltd.

10. Analyse and emphasize the strengths and weaknesses of each of inventory

valuation method. Discuss scenarios where one method might be more suitable

than others.

11. Explain the rationale of each method and its implications on inventory control.

Student’s Book Form Five

72

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 72

ACCOUNTANCY_DUMMY_23 JUNE.indd 72 23/06/2024 17:35