Page 271 - Accountancy_F5

P. 271

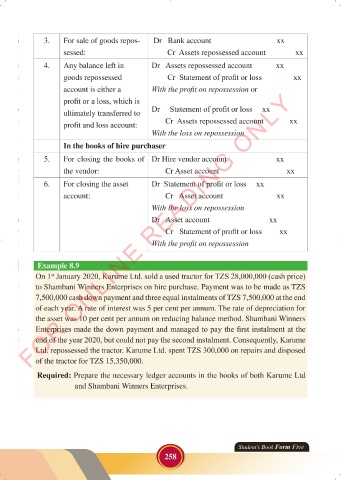

3. For sale of goods repos- Dr Bank account xx

sessed: Cr Assets repossessed account xx

4. Any balance left in Dr Assets repossessed account xx

goods repossessed Cr Statement of profit or loss xx

account is either a With the profit on repossession or

FOR ONLINE READING ONLY

profit or a loss, which is

ultimately transferred to Dr Statement of profit or loss xx

profit and loss account: Cr Assets repossessed account xx

With the loss on repossession

LANGUAGE EDITING

In the books of hire purchaser

5. For closing the books of Dr Hire vendor account xx

the vendor: Cr Asset account xx

6. For closing the asset Dr Statement of profit or loss xx

account: Cr Asset account xx

With the loss on repossession

Dr Asset account xx

Cr Statement of profit or loss xx

With the profit on repossession

Example 8.9

On 1 January 2020, Karume Ltd. sold a used tractor for TZS 28,000,000 (cash price)

st

to Shambani Winners Enterprises on hire purchase. Payment was to be made as TZS

7,500,000 cash down payment and three equal instalments of TZS 7,500,000 at the end

of each year. A rate of interest was 5 per cent per annum. The rate of depreciation for

the asset was 10 per cent per annum on reducing balance method. Shambani Winners

Enterprises made the down payment and managed to pay the first instalment at the

end of the year 2020, but could not pay the second instalment. Consequently, Karume

Ltd. repossessed the tractor. Karume Ltd. spent TZS 300,000 on repairs and disposed

of the tractor for TZS 15,350,000.

Required: Prepare the necessary ledger accounts in the books of both Karume Ltd

and Shambani Winners Enterprises.

Student’s Book Form Five

258

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 258

ACCOUNTANCY_DUMMY_23 JUNE.indd 258 23/06/2024 17:36