Page 273 - Accountancy_F5

P. 273

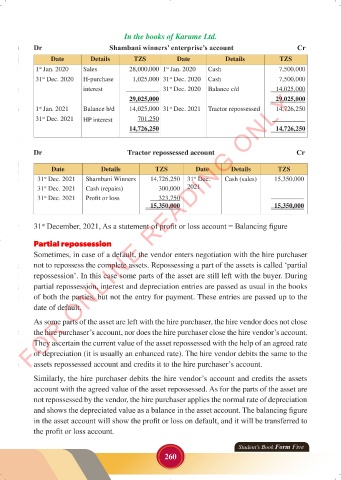

In the books of Karume Ltd.

Dr Shambani winners’ enterprise’s account Cr

Date Details TZS Date Details TZS

st

1 Jan. 2020 Sales 28,000,000 1 Jan. 2020 Cash 7,500,000

st

st

31 Dec. 2020 H-purchase 1,025,000 31 Dec. 2020 Cash 7,500,000

st

st

interest __________ 31 Dec. 2020 Balance c/d 14,025,000

FOR ONLINE READING ONLY

29,025,000 29,025,000

1 Jan. 2021 Balance b/d 14,025,000 31 Dec. 2021 Tractor repossessed 14,726,250

st

st

st

31 Dec. 2021 HP interest 701,250 __________

14,726,250 14,726,250

LANGUAGE EDITING

Dr Tractor repossessed account Cr

Date Details TZS Date Details TZS

31 Dec. 2021 Shambani Winners 14,726,250 31 Dec. Cash (sales) 15,350,000

st

st

31 Dec. 2021 Cash (repairs) 300,000 2021

st

31 Dec. 2021 Profit or loss 323,750 __________

st

15,350,000 15,350,000

31 December, 2021, As a statement of profit or loss account = Balancing figure

st

Partial repossession

Sometimes, in case of a default, the vendor enters negotiation with the hire purchaser

not to repossess the complete assets. Repossessing a part of the assets is called ‘partial

repossession’. In this case some parts of the asset are still left with the buyer. During

partial repossession, interest and depreciation entries are passed as usual in the books

of both the parties, but not the entry for payment. These entries are passed up to the

date of default.

As some parts of the asset are left with the hire purchaser, the hire vendor does not close

the hire purchaser’s account, nor does the hire purchaser close the hire vendor’s account.

They ascertain the current value of the asset repossessed with the help of an agreed rate

of depreciation (it is usually an enhanced rate). The hire vendor debits the same to the

assets repossessed account and credits it to the hire purchaser’s account.

Similarly, the hire purchaser debits the hire vendor’s account and credits the assets

account with the agreed value of the asset repossessed. As for the parts of the asset are

not repossessed by the vendor, the hire purchaser applies the normal rate of depreciation

and shows the depreciated value as a balance in the asset account. The balancing figure

in the asset account will show the profit or loss on default, and it will be transferred to

the profit or loss account.

Student’s Book Form Five

260

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 260

ACCOUNTANCY_DUMMY_23 JUNE.indd 260 23/06/2024 17:36