Page 42 - Book-keeping for Secondary Schools Student’s Book Form One

P. 42

Book-Keeping for Secondary Schools

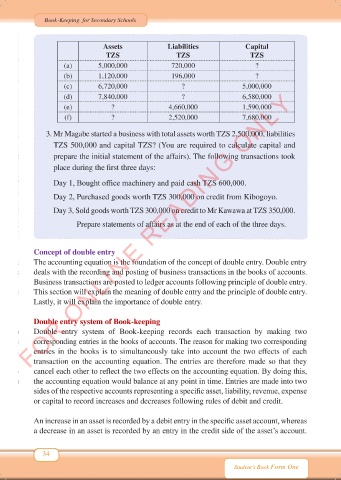

Assets Liabilities Capital

TZS TZS TZS

(a) 5,000,000 720,000 ?

(b) 1,120,000 196,000 ?

(c) 6,720,000 ? 5,000,000

FOR ONLINE READING ONLY

(d) 7,840,000 ? 6,580,000

(e) ? 4,660,000 1,590,000

(f) ? 2,520,000 7,680,000

3. Mr Magabe started a business with total assets worth TZS 2,500,000, liabilities

TZS 500,000 and capital TZS? (You are required to calculate capital and

prepare the initial statement of the affairs). The following transactions took

place during the first three days:

Day 1, Bought office machinery and paid cash TZS 600,000.

Day 2, Purchased goods worth TZS 300,000 on credit from Kibogoyo.

Day 3, Sold goods worth TZS 300,000 on credit to Mr Kawawa at TZS 350,000.

Prepare statements of affairs as at the end of each of the three days.

Concept of double entry

The accounting equation is the foundation of the concept of double entry. Double entry

deals with the recording and posting of business transactions in the books of accounts.

Business transactions are posted to ledger accounts following principle of double entry.

This section will explain the meaning of double entry and the principle of double entry.

Lastly, it will explain the importance of double entry.

Double entry system of Book-keeping

Double entry system of Book-keeping records each transaction by making two

corresponding entries in the books of accounts. The reason for making two corresponding

entries in the books is to simultaneously take into account the two effects of each

transaction on the accounting equation. The entries are therefore made so that they

cancel each other to reflect the two effects on the accounting equation. By doing this,

the accounting equation would balance at any point in time. Entries are made into two

sides of the respective accounts representing a specific asset, liability, revenue, expense

or capital to record increases and decreases following rules of debit and credit.

An increase in an asset is recorded by a debit entry in the specific asset account, whereas

a decrease in an asset is recorded by an entry in the credit side of the asset’s account.

34

Student’s Book Form One

Book Keeping Form 1 New 2024 FINAL.indd 34 18/10/2024 10:14