Page 43 - Book-keeping for Secondary Schools Student’s Book Form One

P. 43

Application of the double entry system

This rule is applied in recording increases and decreases in assets as a starting point.

It also find out the debit and credit rules for the rest of the elements in the accounting

equation. For example, liabilities are on the opposite side of assets in the accounting

equation; therefore, increase in a liability will be recorded on the credit side of the

specific liability account, while a decrease in a liability is recorded by a debit entry in

its account.

FOR ONLINE READING ONLY

The same reasoning will be used for the rest of the items or elements in the accounting

equation. You can quickly do this in relation to the other elements before looking at the

following table. The table summarises the entries for decreases and increases on each

of the elements of the accounting equation. Mastering these rules is very important

because every transaction that you are going to record in the course of your studies in

Book-keeping and Accountancy in general will follow the same rules.

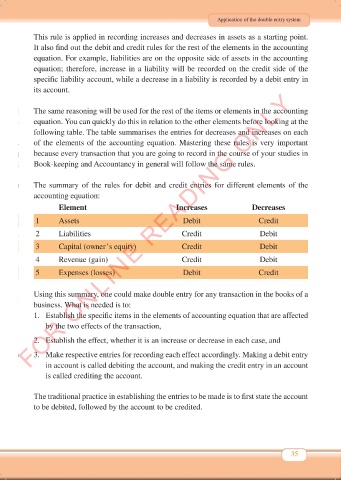

The summary of the rules for debit and credit entries for different elements of the

accounting equation:

Element Increases Decreases

1 Assets Debit Credit

2 Liabilities Credit Debit

3 Capital (owner’s equity) Credit Debit

4 Revenue (gain) Credit Debit

5 Expenses (losses) Debit Credit

Using this summary, one could make double entry for any transaction in the books of a

business. What is needed is to:

1. Establish the specific items in the elements of accounting equation that are affected

by the two effects of the transaction,

2. Establish the effect, whether it is an increase or decrease in each case, and

3. Make respective entries for recording each effect accordingly. Making a debit entry

in account is called debiting the account, and making the credit entry in an account

is called crediting the account.

The traditional practice in establishing the entries to be made is to first state the account

to be debited, followed by the account to be credited.

35

Book Keeping Form 1 New 2024 FINAL.indd 35 18/10/2024 10:14